Skip to content

Skip to content

Anand Ashok

March 19, 2026

Anand Ashok

March 19, 2026

Fintech software development empowers businesses to create crucial financial services, enabling enterprises to create payment gateways, lending platforms, digital wallets, and compliance-ready systems. These systems need to be fast, resilient, secure, and absolutely fail-proof. There is zero room for errors, as a single delay in a payment transaction can cost millions, while if a digital wallet is not secure enough, it can attract lawsuits.

As such, it’s no surprise that the fintech market is growing. According to Market Data Forecast, the global fintech market is valued at $340 billion in 2025 and projected to surge to $1.5 trillion by 2030, growing at a 25% CAGR. For B2B leaders in banking, insurance, and retail, investing in fintech software development is no longer optional, but a requirement to stay competitive.

In this guide, we will dissect fintech software development by understanding how it works, why it is beneficial for your business, and exploring the cost and development elements in detail.

What is Fintech Software Development?

Fintech software development is the process of creating digital systems that provide key financial services such as payments, banking, lending, investing, insurance, and regulatory compliance. It integrates AI, blockchain, and cloud computing to handle high-volume transactions, while adhering to strict regulatory compliance.

To put it simply, fintech software development transforms raw financial data into actionable platforms. It is an innovative process that simplifies financial services so business operations can run smoothly and without friction. For instance, a neobank app might process 10,000 transactions per minute, using microservice architecture, something that’s impossible to perform with legacy systems.

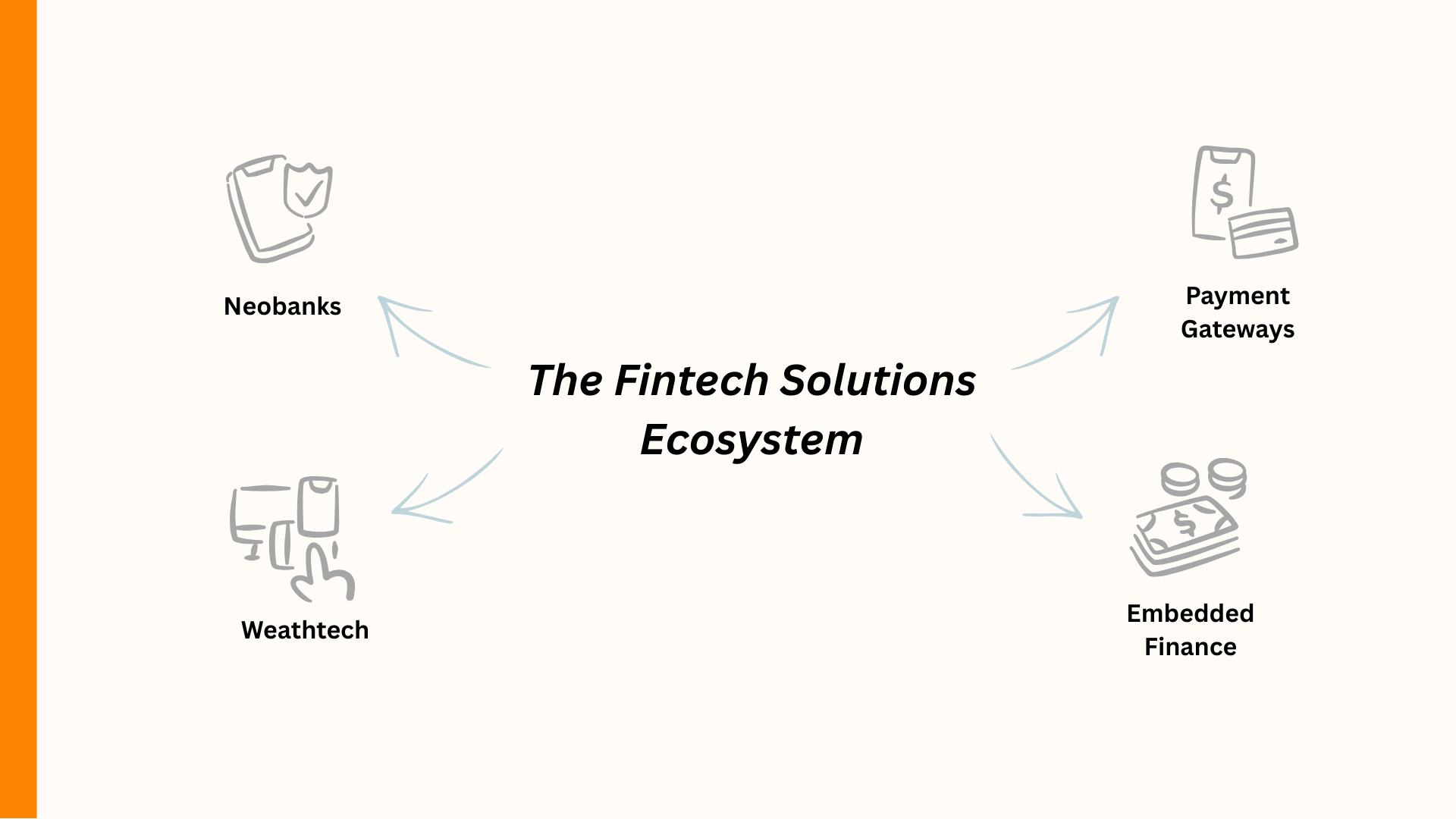

Types of Fintech Solutions:

Fintech software spans multiple categories, each addressing a specific B2B pain point, and each type has its own unique requirements and complexities:

- Digital Wallets: Contactless, e-commerce, mobile wallets

- Banking Platforms: Challenger banks & neobanks

- Payment Gateways & POS

- Insurtech & RegTech Tools

- Investment & Wealthtech Apps

- Lending & Credit Platforms

- Embedded Finance in non-financial apps

Why Businesses Invest in Fintech Software?

The global financial industry is shifting from rapid growth to more sustainable and strategic expansion. Financial markets have always been competitive, where the only way to survive and retain your seat is to innovate and provide the best financial services.

The onset of AI has opened opportunities for businesses looking to innovate and perfect their services with new technologies like machine learning algorithms, natural language processing, and predictive analytics systems, which allow real-time fraud detection, personalized wealth management, and intelligent customer experience. This is evident by the growing adoption of AI in fintech software development, where Market Data Forecast reports a 41.2% increase in AI adoption in fintech from 2025 to 2033.

As financial interactions move faster, become more digital, and are more embedded into everyday products, companies that fail to modernize their financial systems quickly fall behind, proving that firms are increasingly relying on fintech software development to create digital services that make them competitive.

Let’s look at some of the key benefits of fintech software and what it means for businesses:

- Expectations of quick, digital-first financial

services:

Today’s users expect real-time payments, seamless onboarding, and complete transparency. Fintech software enables speed, clarity, and reliability that legacy systems simply can’t match.

- Reduced operational costs and human error:

Fintech software development includes features and integrations that automate payments, reconciliation, reporting, and fraud checks, leading to a reduction in processing costs and human errors.

- Unlocking new revenue streams:

Embedding financial services into digital products, such as payments, lending, wallets, or insurance, taps into rapidly expanding opportunities that generate new revenue streams for businesses, ensuring long-term profitability and growth.

- Improved and personalized customer experience:

A strong majority of financial services customers now expect personalized digital experiences, and fintech platforms are essential to deliver on that. According to Coin Law, around 74% of customers expect personalized services by 2025, making tailored financial experiences a key differentiator in retention and loyalty.

- Faster decision-making and scalability:

Real-time financial data and analytics help businesses understand user behavior, cash flow, and risk exposure, empowering better pricing, segmentation, and risk management. Meanwhile, fintech architectures built for scale handle variable demand without breaking, unlike legacy systems.

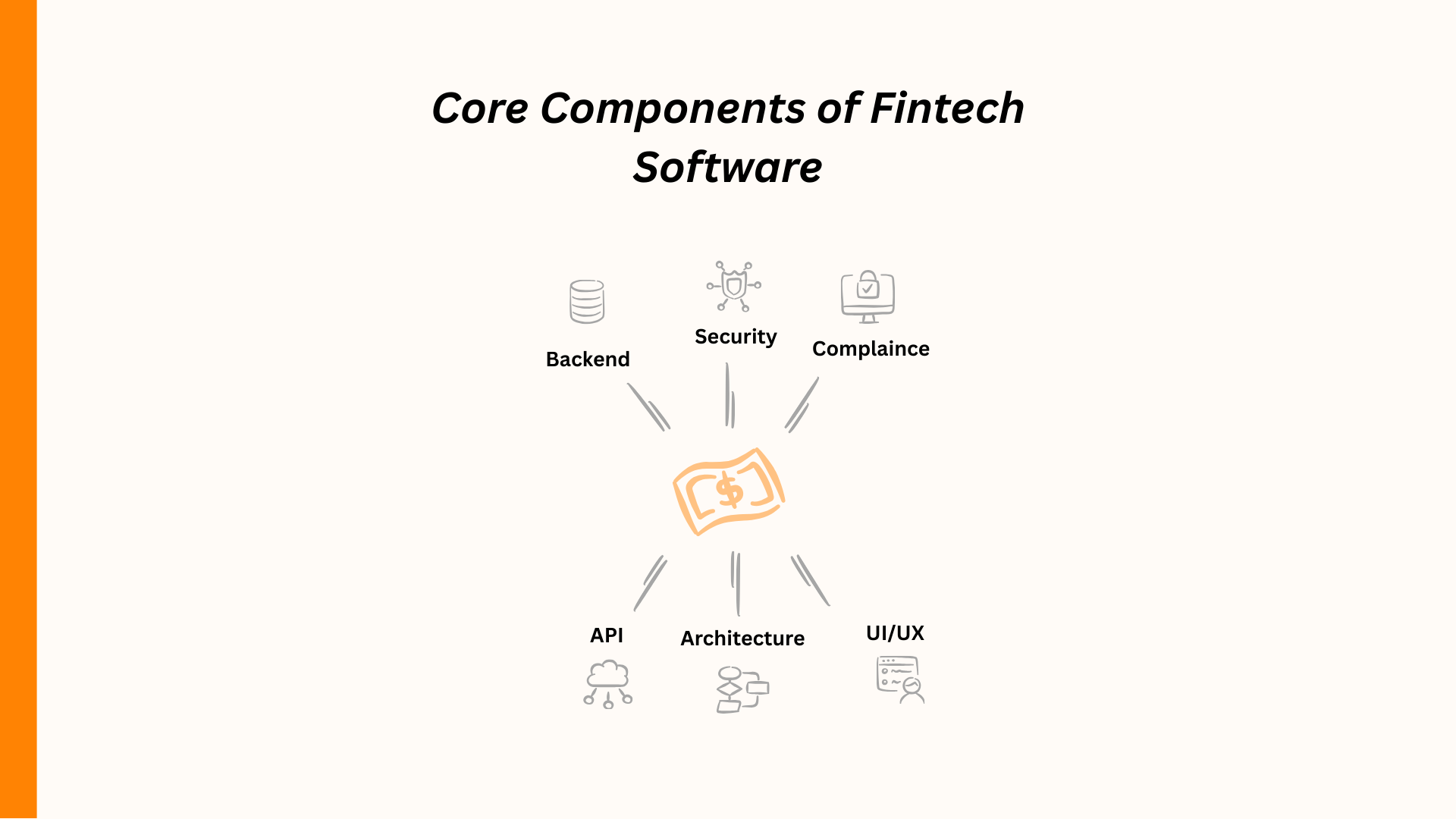

What Are The Core Components of Fintech Software?

Fintech software development is more than just building an app or software. Its success is defined by systems that process money accurately, enforce rules consistently, and withstand regulatory scrutiny. Each core component exists to solve a specific financial or operational risk. If any one of these components is weak, the entire platform becomes unreliable.

The following are the core components of fintech software that make it work:

1. Backed and Business Logic

The backend is the operational core of fintech software. It executes all financial actions, from transaction processing, balance updates, fee calculations, and approvals, to payment settlements. The backend layer allows the fintech software to handle and operate sensitive workflows where order, timing, and accuracy are critical.

This layer also enforces business rules and logic such as transaction limits, credit checks, compliance conditions, and exception handling. A well-designed fintech backend can ensure consistent outcomes for every financial operation, making scalability and reliability possible.

2. Security Infrastructure

Security is quintessential for fintech software, as it ensures the protection of financial data, user identities, and transaction integrity from fraud and unauthorized access. Financial firms operate in high-risk and highly regulated environments, where security is non-negotiable. This requires security components to be directly embedded in the architecture.

The security component of fintech software is responsible for encryption, authentication, access control, and fraud detection. It also enables continuous monitoring to identify abnormal behavior in real time. A single security failure can expose user funds, sensitive information, invite scrutiny from regulators, and damage trust. Therefore, strong security is not a feature or competitive advantage but a basic requirement.

3. Compliance & Regulatory Modules

Compliance and regulatory modules ensure fintech software operates within the legal and regulatory framework of the region. This module allows for automation of KYC procedures, AML checks, transaction monitoring, data protection, and regulatory reporting. With the increase in transaction volumes, manual compliance checks become an inconvenience, making automated compliance procedures essential.

These modules reduce legal risk while enabling faster onboarding and geographic expansion, because in fintech, compliance must be an in-built system function.

4. APIs & Third-Party Integrations

Fintech software operates within connected systems. APIs enable financial applications to interact with banks, payment processors, identity verification services, credit bureaus, and other third-party systems.

A strong API architecture is protected with strong authentication mechanisms like OAuth 2.0 and OpenID Connect to prevent security risks, downtimes, and operational overheads. It also allows fintech platforms to scale, adapt, and expand without destabilizing the core system.

5. Scalability & Performance Architecture

Scalability determines whether a fintech software can grow safely under increasing transaction volumes and user load. Since financial platforms often experience sudden spikes in transactions, this module ensures that the software can adapt to those changes and grow with the demand, and not work against it.

Performance speed is another important factor in fintech software development. Customers want fast transaction speeds, low latency, and a smooth experience. To achieve high performance, even during peak times, fintech software is integrated with specialized hardware acceleration (e.g., FPGAs), kernel bypass networking, colocation for ultra-low latency access to exchanges, and leveraging edge computing to process data closer to the source. This allows for a smooth customer experience and an improved brand image.

6. User Experience (UX) Component

User experience (UX) and User Interface (UI) act as a bridge between the technical backend and the users. This component is responsible for how people interact and use the financial product, directly influencing adoption, trust, and error rates. This is evident in a report from The Financial Brand, which found that 73% of online-only bank users would switch banks for a better digital experience.

A good fintech UX is more than just being visually appealing; it focuses on clarity, transparency, and intent-driven actions. Users must clearly understand what they are doing with their money, because poor UX can increase abandonment, support overhead, and compliance risk.

How is Fintech Software Developed?

Now that we’ve understood what fintech software development means and the key components that make it work, let’s understand how fintech software is developed.

The fintech software development process is a risk-driven and compliance-aware process, where every step is designed to reduce financial, security, and regulatory exposure while ensuring the product can scale reliably.

Below are the key stages of the fintech software development process:

1. Discovery & Identifying Requirements

The development process begins with understanding what the fintech software must do and what it should avoid doing. This stage focuses on understanding business objectives, doing thorough market research, creating a target user base, and determining regulatory needs.

This step lays the foundation for the entire development process, ensuring each step follows a clear, directional order that aligns with the end goal.

2. Architecture Design & Technology Planning

This step involves building the core functionality of a fintech software. This involves defining how the system will handle transactions, data storage, user interface, integrations, security, and scalability.

A good software architecture enables growth, resilience, and faster future development, increasing scalability and reducing long-term operating costs.

3. UI/UX Design

In this stage, user flows are designed for onboarding, transactions, approvals, and error handling, ensuring users understand financial actions before confirming them. These designs are tested and then developed at the backend.

Interface design is critical to a smooth customer experience and to how users interact with fintech software. As such, a good design for a fintech software should focus on clarity, functionality, and simplicity, without complicating the process.

4. Development & Integration

Once the technical requirements and UI/UX designs have been defined, the development process takes place to build the system and core functionality of a fintech software. This involves building the backend logic, security mechanisms, compliance modules, and APIs, while also integrating payment gateways and KYC providers.

5. Security, Testing & Compliance Validation

Before releasing the fintech software to the users, it is essential to conduct thorough testing to verify its functionality, reliability, and security. Systems are tested for security vulnerabilities, data integrity, transaction accuracy, and regulatory compliance. This includes penetration testing, audit readiness checks, and scenario-based validations.

This stage ensures that the fintech software is secure, functional, and compliant with regulatory requirements.

6. Deployment & Monitoring

Following successful testing, the fintech software is deployed into production in a carefully controlled environment. Real-time monitoring tracks performance, transaction health, error rates, and security signals from day one.

This stage involves continuous monitoring of the launched software to observe how customers are using the software.

7. Maintenance, Updates & Optimization

Fintech software requires ongoing maintenance and updates to maintain security, functionality, and compliance.

This phase involves providing troubleshooting solutions, offering new feature enhancements, and adapting to changing regulatory requirements. Usually, a dedicated team is there to offer ongoing support and regular maintenance of the software.

What are the Cost Considerations for Fintech Software Development?

The cost of developing fintech software depends on multiple factors and components. While the project prices vary, depending on the requirements, there are some considerations that remain fixed and determine the overall cost of fintech software development.

Understanding these cost drivers helps businesses plan realistically and avoid underestimating long-term investment.

- Type of fintech product:

The cost of fintech software depends on the nature of the product itself. Payments, lending, neobanking, and wealth management software all have different backend complexity and regulatory exposure. Choosing the type or types of fintech software determines the overall cost of the project.

- Security & compliance requirements:

Fintech software operates in a highly-regulated environment that demands robust security procedures and compliance norms. Mandatory elements such as KYC, AML, data encryption, audit logging, and regulatory reporting significantly increase development effort. These components are not optional and count as baseline costs.

- Third-party integrations:

Fintech software often requires integrations with payment gateways, CRMs, banking APIs, and other systems, increasing the complexity of the software and impacting the development cost.

- Scaling & upgrading costs:

Your fintech software should be scalable enough to handle high volumes of transactions and data. Costs associated with scaling the fintech software infrastructure, adding new features, and software upgrades must be taken into account.

- Geographic and regulatory scope:

Operating across multiple countries increases compliance, reporting, and localization requirements, which directly impact development and maintenance costs. Similarly, outsourcing the development of fintech software to cost-effective countries can greatly reduce project costs. Visit this blog on “Why Outsource FinTech Software Development to India?” to get a more in-depth understanding of how outsourcing impacts the overall cost.

- Maintenance & support costs:

Ongoing maintenance and support include bug fixes, performance optimization, security updates, and regulatory changes. These recurring costs often get underestimated during initial planning.

To have a more complete understanding of the cost aspect of fintech software development and how each consideration impacts the overall project budget, check out our blog on fintech software development cost.

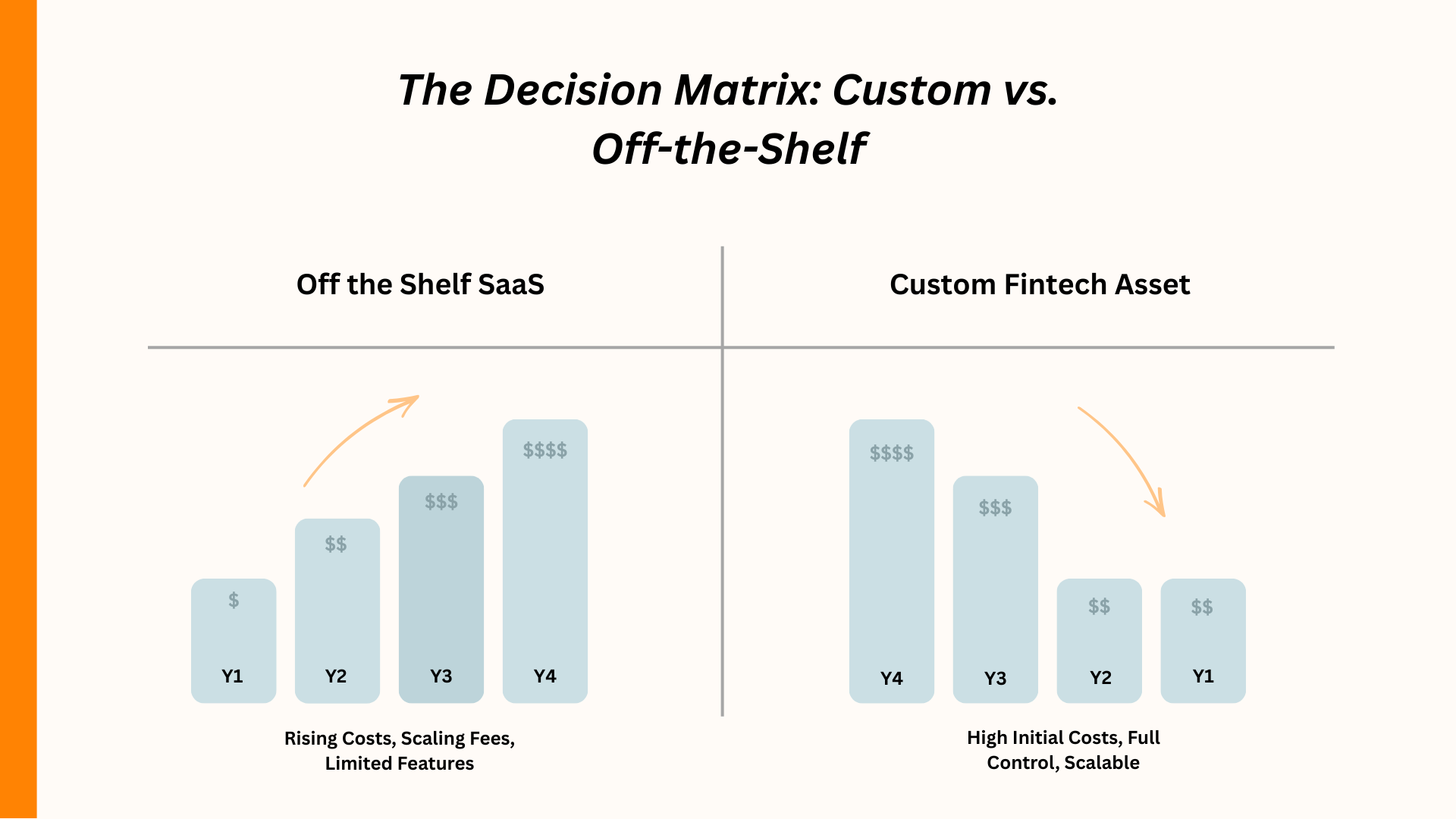

How To Choose The Right Fintech Software Approach?

Choosing the right fintech software approach depends on how well it aligns with your business model, regulatory exposure, and long-term growth plans. Use the following checklist to make an informed decision:

- Centrality of the software to your business

If the fintech software is your primary product, then you need complete control over architecture, data, and workflows. If it’s a supporting tool, then constraints or some limitations are acceptable.

- Regulatory exposure and change frequency

If your software operates in a heavily-regulated environment or runs multi-country operations, then you need software that can adapt quickly to regulatory updates.

- Scalability and transaction load

Fintech software needs to handle seasonal spikes and regular high volumes of transactions. Many ready-made fintech solutions are limited in their capacity to handle large volumes or are expensive to upgrade.

- Long-term ownership cost

Instead of focusing on upfront cost, evaluate data ownership, vendor lock-in, scaling fees, and the ability to evolve the product without rebuilding it later.

The above checklist gives you an idea of the factors you need to consider before choosing a particular type of fintech software. However, the choice eventually comes down to either a custom-made fintech software or an off-the-shelf fintech solution. To get a better understanding of which one’s right for you, check out our article on “Custom FinTech Software Development vs Ready-Made Solutions: Which is Better For You?”

Conclusion

Fintech software development is not just a technical exercise, but a strategic one. It requires you to have a deep understanding of the business goal, regulatory framework, customer expectations, and long-term objectives. Every stage, from planning to deployment, is essential to the success of the end product, which requires you to identify key features, prioritize security, and select the best software type that aligns with your goals.

In this fintech software development guide, we have explained that whether you are launching a new fintech platform or modernizing an existing one, investing in the right development approach early creates a foundation that supports growth, resilience, and innovation in an increasingly competitive financial ecosystem.