Skip to content

Skip to content

Anand Ashok

January 22, 2026

In a rapidly evolving world of financial technology, choosing whether to build custom fintech software or buy a ready-made solution is one of the most strategic decisions a business can make. This decision will affect the budget, scalability, regulatory compliance, customer experience, and long-term competitive advantage of the firm.

This article breaks down the differences, pros and cons, cost implications, and decision frameworks to help businesses make the right choice with confidence.

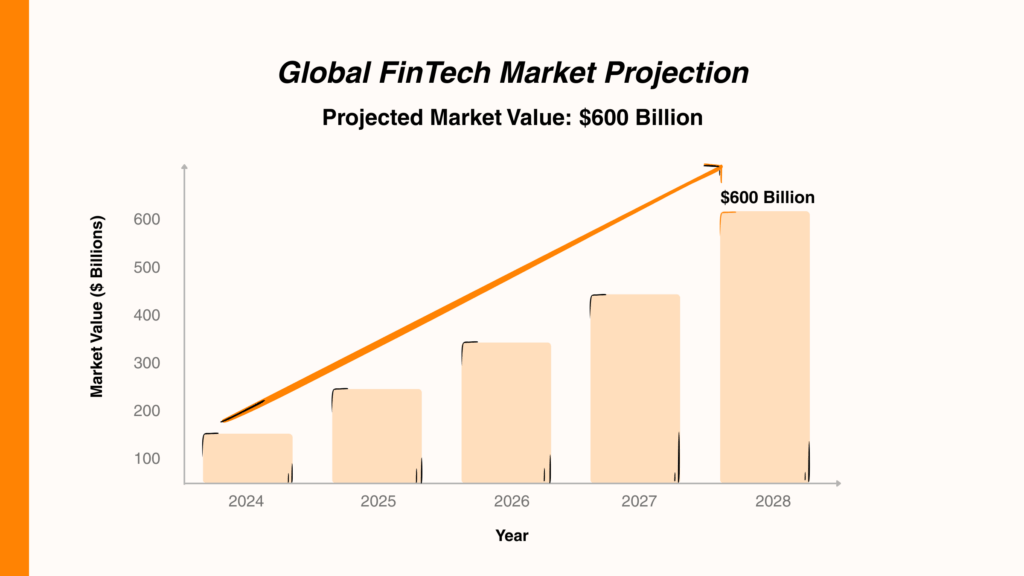

According to recent fintech market reports by Companies History, the global fintech market is projected to reach $460.76 billion in 2026, driven by the increasing adoption of digital banking, payments, lending platforms, and AI-powered financial services. Companies investing in FinTech software are expected to gain stronger operational efficiency, customer reach, and long-term business growth.

This change in market dynamics demands that Fintech firms make a clear decision on what kind of Fintech software they should invest in, which aligns with their business strategy.

The difference between custom and ready-made FinTech software goes far beyond initial setup. It influences the process of development, adjustment, and competition of a business in the long run. The comparison is clear and detailed across the key decision factors as illustrated below.

Ready-made software is easy to deploy since it is already tested and built. It takes less time to set up businesses, and the level of setup is minimal. This is why it is appropriate in businesses that require a quick launch or testing an idea. Custom software, on the other hand, takes time to plan, design, develop, and test. Although the initial rollout is slower, it enables the business to create precisely what it needs initially.

Ready-made solutions are typically less expensive in terms of initial cost, which may be subscription or licensing fees. Nonetheless, as time goes on, the cost may rise as a result of recurring payments and other features,s as well as scaling constraints.

Custom software is a more expensive investment, yet the costs over the long term may be more predictable. Companies save money by not paying recurring licensing fees and have the option to upgrade and change the software as they wish.

Ready-made platforms are designed to satisfy general regulatory requirements, although they might not be able to promptly adapt to new or region-specific regulations. Businesses may have to wait for the vendor to release updates. Custom software enables businesses to create systems that address certain regulatory requirements. It further simplifies the process of updating processes in a quick manner as regulations change.

Standard integrations are usually supported by ready-made software. However, it may have limitations when connecting with unique or legacy systems. Custom solutions can be built to integrate seamlessly with existing systems, third-party services, and internal tools. This allows more flexibility and guarantees that there is a smoother flow of data throughout the organization.

With ready-made platforms, data is often stored on the vendor’s infrastructure. Although companies have access to their data, they may not have complete control over the storage and management of their information. Bespoke software provides complete authority over the storage, access, and management of data. This is especially relevant to the businesses that deal with sensitive financial data.

Off-the-shelf solutions may lead to a dependency on the vendor. Changing providers can be complicated, expensive, and time-consuming because of data transfer and adjustments to the system. This risk is minimized by custom software, since businesses own the system and can modify or migrate it as they need, without being dependent on a single provider.

The pre-coded programs have generic features that most of their rivals are likely to utilize. This may result in businesses failing to be unique in the market. Bespoke software helps businesses to create distinctive features and user experiences, which reflect their brand and strategy. This assists in building a more competitive edge.

In short, standard software is fast and easy to use, whereas custom software is controllable and flexible and offers a long-term strategic value. The correct decision will be based on the priorities, resources, and growth plans of the business.

Factor | Ready-Made Software | Custom Software |

Time to Market | Fast deployment with minimal setup; ideal for quick launches and MVP testing | Longer build cycle involving planning, design, development, and testing; slower initial rollout |

Total Cost of Ownership | Lower upfront cost via subscriptions or licensing; costs increase over time due to recurring fees, add-ons, and scaling limits | Higher initial investment; more predictable long-term costs with no licensing fees and full control over upgrades |

Compliance Adaptability | Built for general regulations; region-specific updates depend on vendor release timelines | Designed for specific regulatory needs from day one; updates can be implemented as regulations evolve |

Integration Ecosystem | Supports standard integrations; may struggle with legacy systems or niche tools | Built to integrate with existing infrastructure and third-party services, ensures smoother data flow |

Data Ownership | Data stored on vendor infrastructure; limited control over storage and management | Full ownership and control over data storage, access, and governance |

Vendor Lock-in Risk | High dependency on vendor; switching is complex and costly | Minimal lock-in; full control allows independent modification or migration |

Product Differentiation | Generic features shared across competitors; limited differentiation | Fully customizable features aligned with business strategy; stronger competitive edge |

Best Suited For | Startups testing ideas, businesses with standard workflows, or limited technical resources | Businesses with complex needs, regulatory demands, sensitive data, or long-term product vision |

Before you decide on which fintech software to go with, understanding the advantages and disadvantages of them is a major factor. This will help you make an informed decision on which software is best for your business goals.

Pros:

Aspect | Custom FinTech Software |

Customization | Unlimited |

Time to market | Months |

Cost | High upfront |

Ownership | Owned by you |

Updates & maintenance | Your responsibility |

Scalability | High |

Cons:

Pros:

Cons:

Dimension | Custom FinTech Software | Ready-Made FinTech Software |

Upfront Cost | High ($100K–$500K+) | Low ($0–$50K setup or subscription) |

Ongoing Cost | Predictable (~15–20% annually) | Escalating (subscriptions, add-ons, tier upgrades) |

Time to Market | Slow (4–8+ months) | Fast (days to weeks) |

Customization | Full control; built exactly for your workflows | Limited; you adapt to the software |

Scalability | High; scales with architecture and infra | Limited by vendor pricing tiers and constraints |

Integration | Built to fit your ecosystem natively | Often requires middleware and workarounds |

Ownership | Full ownership of code and data | No ownership; access tied to subscription |

Maintenance | Your responsibility (or dev partner) | Vendor-managed |

Security & Compliance | Fully customizable to regulatory needs | Standardized; depends on vendor updates |

Vendor Dependency | None | High (lock-in, pricing changes, risk exposure) |

Competitive Advantage | Strong, unique features and workflows | Weak; same tools used by competitors |

Long-Term ROI | High (cost stabilizes, value compounds) | Declines over time as costs increase |

Best Fit | Scaling businesses, complex operations, and long-term strategy | Startups, simple use cases, quick deployment needs |

If you want to learn more about FinTech software development, read this blog, “A Complete Guide to Fintech Software Development”.

Cost is usually the first question in this decision, and it is also the most misunderstood one. Ready-made software looks cheaper on day one. Custom software looks expensive. But when you factor in recurring fees, scaling costs, integration overhead, and the compounding effect of vendor lock-in, the real picture looks quite different. Here is an honest breakdown.

Cost Category | Custom Fintech Software | Ready-Made Fintech Software |

Upfront Build / Setup | $20,000 – $150,000+ (₹16.6L – ₹1.24Cr+) depending on complexity | $0 – $5,000 (₹0 – ₹4.15L) for onboarding and initial configuration |

Monthly Subscription | None | $500 – $15,000/month (₹41,500 – ₹12.45L/month) depending on tier and users |

Per-User / Tiered Costs | None — you own the system | $10 – $100 per user/month (₹830 – ₹8,300); costs scale with team size |

Integration Fees | Built into the development scope | $2,000 – $20,000 (₹1.66L – ₹16.6L) per integration via middleware or vendor APIs |

Compliance and Security | Designed into the system from day one | Often sold as add-ons; $200 – $2,000/month (₹16,600 – ₹1.66L/month) extra |

Annual Maintenance and Support | $4,000 – $15,000/year (₹3.32L – ₹12.45L); predictable and controlled | Included in subscription, but major updates or customizations are chargeable |

Customization Costs | Already built to your specifications | $5,000 – $50,000+ (₹4.15L – ₹41.5L+) for modifications beyond standard feature set |

Migration is an expense most businesses do not think about until they are stuck, and by then, it is expensive.

Custom Fintech Software: When migrating to or from a custom system, costs are relatively contained because you own the codebase and the data. A typical migration, like moving data, reconfiguring environments, testing, and validating, runs between $5,000 – $25,000 (₹4.15L – ₹20.75L). The variables are data volume, system complexity, and the extent of integration rewiring required.

Ready-Made Fintech Software: Migrating away from a SaaS platform is considerably more painful. Vendors often store data in proprietary formats, charge data export fees, and provide limited migration support. Factor in data restructuring, rebuilding integrations on the new platform, staff retraining, and potential downtime, and costs typically land between $10,000 – $50,000+ (₹8.3L – ₹41.5L+). For businesses that have been on the same SaaS platform for several years with deeply embedded workflows, this number can climb further.

Learn more about why businesses outsource fintech software development to India in this blog, “Why Outsource FinTech Software Development to India?”

This is where the real difference between the two options shows up.

Custom Fintech Software: Hidden costs are largely maintenance-related, like bug fixes, security patches, minor feature updates, and infrastructure management. A reasonable estimate is 10–20% of the initial development cost per year. On a $100,000 (₹83L) build, that means $10,000 – $20,000 (₹8.3L – ₹16.6L) annually. These costs are predictable and within your control, and they do not scale with your user base or revenue.

Ready-Made Fintech Software: Hidden costs here are structural. Most SaaS fintech platforms are designed to upsell. As your business grows, you will hit tier ceilings that force plan upgrades. You will add integrations that require middleware. You will need compliance modules, advanced reporting, or white-labeling. A realistic estimate is 20–50%+ of your base subscription cost annually in additional charges. A business paying $2,000/month (₹1.66L/month) at baseline can realistically spend $2,800 – $3,500/month (₹2.32L – ₹2.9L/month) once the full cost stack is accounted for.

This is where the comparison becomes most instructive. Looking at total spend over five years rather than just year one changes the picture significantly.

Component | Custom Fintech Software | Ready-Made Fintech Software |

Initial Build / Setup | $80,000 – $150,000 (₹66.4L – ₹1.24Cr) | $1,000 – $5,000 (₹83K – ₹4.15L) |

Subscription Costs (5 years) | None | $30,000 – $180,000 (₹24.9L – ₹1.49Cr) |

Scaling / User Growth | No per-user fees; infrastructure scales at low marginal cost | $10,000 – $60,000+ (₹8.3L – ₹49.8L+) in tier upgrades and seat additions |

Integrations and Middleware | Included in build; minimal ongoing cost | $10,000 – $40,000 (₹8.3L – ₹33.2L) across the period |

Customization | Built to spec; changes are straightforward | $15,000 – $60,000+ (₹12.45L – ₹49.8L+) for modifications beyond defaults |

Maintenance and Support | $40,000 – $75,000 (₹33.2L – ₹62.25L) over 5 years | Included in subscription, but dependent on vendor support quality |

Estimated 5-Year TCO | $140,000 – $275,000 (₹1.16Cr – ₹2.28Cr) | $66,000 – $345,000+ (₹54.8L – ₹2.86Cr+) |

The ready-made option appears significantly cheaper at face value, but the upper range tells the real story. SaaS costs inflate over time with tier upgrades, additional user seats, integration middleware, storage overages, and mandatory plan changes as vendors restructure their pricing. A business that starts at $1,500/month (₹1.24L/month) on a SaaS platform is unlikely to still be paying that rate in year four.

Custom software’s higher upfront cost is front-loaded and then largely fixed. You are not subject to vendor pricing decisions, and your ongoing costs do not move in lockstep with your user count or revenue growth.

Get an in-depth understanding of fintech software development cost and features in this blog, “FinTech Software Development: Key Features, Cost & Technology Stack”.

Use custom fintech software if:

Choose ready-made fintech solutions if:

We’ve created a structured framework to help you make an informed decision on which fintech software is right for your organization, based on your goals, needs, budget, operational requirements, and other relevant factors.

Decision Area | Choose Custom Software If | Choose Ready-Made Software If |

Primary Goal | Fintech is your core product and long-term competitive advantage | Fintech is a supporting function, not your main differentiator |

Product Needs | Your workflows, logic, or features are unique to your business model | Standard features (payments, ledgers, KYC) cover 80%+ of your needs |

Time to Launch | You can commit to a 4–8 month build cycle to get it right | You need to launch in under 8 weeks to test or capture a market opportunity |

Budget Structure | You can invest upfront and want predictable long-term costs | You prefer low upfront cost and can handle ongoing subscription expenses |

Compliance Requirements | You operate across multiple jurisdictions with complex or evolving regulations | Your compliance needs are standard and handled by existing platforms |

Scalability Expectations | You expect rapid growth, high transaction volume, or complex processing | Growth is gradual and some limitations are acceptable |

Cost Model Preference | You want stable costs that don’t scale with users or revenue | You’re comfortable with variable pricing (per user, usage, tiers) |

Control & Ownership | You need full ownership of code, data, and infrastructure | You’re fine with vendor-managed systems and limited backend control |

Integration Depth | You require deep, custom integrations with internal or legacy systems | Standard API integrations are sufficient |

Competitive Positioning | Your advantage comes from unique product capabilities and UX | Your edge is distribution, branding, or service—not software |

If most of your answers fall in one column, the decision is clear.

If your answers are split across both columns, you are likely in a transitional phase. The best approach is typically to start with ready-made software to validate your business model, acquire initial users, and learn what actually matters to your market, then plan a custom build once you have the traction, capital, and clarity to justify the investment.

Naturally, there’s no universally “better” option, only what fits your current stage and aligns with your long-term goals. Ready-made fintech software makes sense when speed, lower upfront costs, and quicker validation from the market matter most. Custom fintech software is the right choice when the product is core to your business, regulatory control is critical, and scalability or differentiation will define your success.

The mistake most fintech teams make is basing their decisions on short-term convenience instead of long-term cost, flexibility, and ownership. Therefore, it is important to evaluate your business maturity, growth trajectory, compliance needs, and 3–5 year cost impact to make a far better decision than chasing trends or price alone.

If building a custom fintech software aligns with your business goals, you can explore more about the fintech software development process, how it’s approached, built, and scaled at Quixta’s FinTech Software Development Services.

Custom fintech software is a better choice when a business needs full control, flexibility, and the ability to scale without restrictions. It allows companies to design features that match their exact processes and customer needs. Ready-made solutions are suitable for businesses that want a quick start with lower initial investment. However, they may limit flexibility and long-term growth. The better option depends on whether the priority is speed or long-term value.

The cost of custom fintech software in 2026 typically ranges between $20,000 and $100,000 or more (₹16 lakh to ₹80 lakh+). The final cost depends on factors such as feature complexity, level of security, integrations, and compliance requirements. More advanced platforms, such as digital banking or lending systems, will fall on the higher end of the range.

Yes, custom fintech software is often more cost-effective over time. While the initial investment is higher, businesses avoid recurring subscription fees, per-user charges, and forced upgrades. Costs remain more predictable, especially as the business scales, making it a strong option for companies planning long-term growth.

Yes, businesses can move from ready-made to custom software as they grow. This is a common approach for startups that initially prioritize speed.

However, migration involves effort, cost, and careful planning, especially when transferring data and ensuring system continuity. Planning this transition early can reduce future challenges.

Custom fintech software usually takes 4 to 8 months or longer to build. The timeline depends on the number of features, design requirements, testing, and compliance needs. More complex platforms may require additional time to ensure accuracy, security, and reliability before launch.

Ongoing maintenance typically costs $4,000 to $10,000 per year (₹3 lakh to ₹8 lakh). This includes system updates, security improvements, performance monitoring, and minor enhancements. These costs are generally predictable and can be planned.

Yes, most ready-made fintech solutions are built with standard security measures and are tested across multiple users.

However, they follow a general approach to security. Businesses with specific or advanced security needs may find custom software more suitable, as it can be designed to meet precise requirements.

As a business grows, ready-made software may face limitations such as restricted features, higher subscription tiers, and difficulty handling increased users or transactions. Companies may also find it harder to adapt the system to new business models or changing customer expectations.

For most startups, ready-made software is a practical starting point because it allows faster launch and lower upfront cost.

Once the business gains traction and clearer requirements, moving to custom software can provide better control, scalability, and long-term value.

Businesses should evaluate factors such as budget, timeline, growth plans, compliance needs, and the importance of product uniqueness. If the goal is quick market entry with limited investment, ready-made software is suitable. If the software is central to the business strategy and requires long-term flexibility, custom development is the better choice.

Anand is a founder and operator with over a decade of hands-on experience building and scaling digital products, SaaS platforms, and growth systems for startups and business houses. He leads a multidisciplinary design and development firm – Quixta, working directly with founders and leadership teams on product strategy, engineering, SEO, and go-to-market execution. Anand’s expertise comes from shipping real products, managing live growth experiments, and advising businesses across industries. His writing is informed by first-hand experience, data from active projects, and lessons learned from building and scaling products in competitive markets.

Complete the form below, and we’ll get back within one business day.